The concept of Web 3.0 is currently being explored

The concept of Web 3.0 is currently being explored in relation to the future of the internet, and is expected to be a significant development in the years ahead. While there is a great deal of attention being paid to emerging technologies such as AI, Blockchain, and IoT, there is a risk that Web 3.0 may be overlooked. This article seeks to provide a broad overview of the potential impact of Web 3.0 on the fintech industry, and how it could influence the growth and evolution of fintech in the months and years to come.

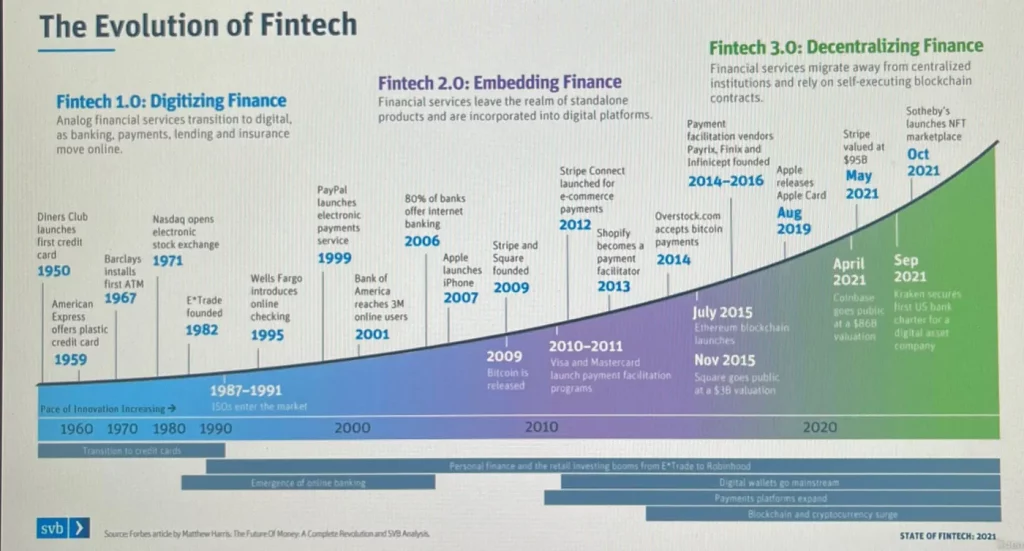

Here is roadmap of the evolution of Fintech for better visualization.

Let’s begin!

Fintech is the name given to a wide range of financial technologies based on emerging internet technologies. This includes, for instance, mobile apps for banking, peer-to-peer lending, crowdfunding (such as Kickstarter), and cryptocurrencies such as Bitcoin. According to research from PwC, around half of people in the U.S. have banked with at least one fintech start-up, and nearly half of quantified self-users use a fintech app on their phones. Yes, it’s still growing fast!

IoT is a technology that allows devices to connect to each other and the internet. The idea is that these devices will be able to communicate with each other, allowing them to work together in order for you to get the most out of your investment in them. For example, if you have an IoT device sitting on the kitchen countertop and another sitting on top of it (like a coffee maker), both devices can communicate with each other via Wi-Fi or Bluetooth so they know what’s going on at any given moment.

This means that instead of having one person make coffee every morning or even two people who live together. You could have multiple coffee makers set up around your house so no matter where you are in relation to one another when making your morning cup (unless someone else had already made theirs), there would always be fresh brew ready for consumption.

Blockchain is a distributed ledger that can be used for transactions, data storage, and smart contracts.

Blockchain has the potential to revolutionize the financial industry by making it more secure, efficient, and transparent. It can also help reduce costs in business processes such as trade finance because all parties involved in an agreement are able to agree on terms beforehand rather than having them negotiated later when they might not have enough information available at that point in time.

AI is going to change the way we interact with our customers. It’s already being used in real-time and will continue to evolve in the future, allowing us to provide proactive solutions that are tailored to individual needs.

AI will also be able to understand customer preferences and provide them with a tailored experience, which can help increase conversion rates as well as reduce customer churn.

AI will be the Future of Intelligent Finance. With the rise of AI, it is likely that the future will be full of intelligent finance. AI will help make more informed decisions and give customers a better experience. For example, you might use an AI-powered chatbot on your website that can answer questions about financial products or help users find the right loan for their needs.

Another way that AI could affect financial services is with automation: as more companies use it within their business processes, they’ll have access to more data than ever before — and this could lead them down paths like using machine learning algorithms or preprogrammed rules (like “if there are five people applying for a loan at once…”). With all this extra information available thanks to automation programs like these becoming popular over time.

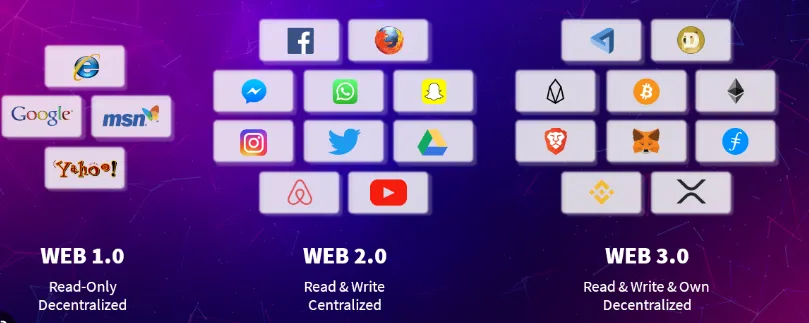

Web 3.0 is going to going to lead the way for blockchain, AI and loT in FinTech. Web 3.0 is the next phase of the Internet, which will be a major step forward for Fintech. This means that we can expect blockchain, AI, and IoT to become increasingly important parts of the future of Fintech as well.

Blockchain has already been used by banks and other financial institutions since 2008 but they are now taking steps towards implementing it on a larger scale within their businesses so they can benefit from its benefits in different ways:

Consumer protection — By using blockchain technology consumers can access their own data without having third parties looking over their shoulders (e.g., Google). In addition, consumers will no longer have to rely on banks or lenders when engaging in financial transactions; this would mean that individuals would have greater control over which companies handle their money (e.g., PayPal).

Web 3.0’s benefits for the FinTech world. The third generation of internet services will change how people, businesses, and regulatory authorities collaborate, creating a more connected and intelligent world for the financial services sector. The following are the primary benefits of Web 3.0 and our new decentralized operating model convergence:

(1) Reliability: Web 3.0 will provide users with a more convenient and user-friendly onboarding experience. Web 3.0 will leverage decentralized networks to ensure that end users always have complete ownership and control over their online data. By reducing the security problems linked with preserving any data, each and every evolution of the Web from this point forward will provide increased dependability for businesses.

(2) Easy of access: One of the most significant advantages of Web 3.0 is the ability for users to access content from anywhere on the planet. It will allow companies involved in loan origination and servicing, BNPL (buy now, pay later), and other operations to readily access information such as the amount of money currently available in an account or information that verifies a person’s identification.

(3) A better client experience: Web 3.0 will help FinTech organizations better understand their clients’ shifting demands and expectations. Businesses can use Web 3.0’s list of contributing technologies to automate procedures for customer journey mapping and more effectively allocate resources in order to better satisfy consumer expectations, boost engagement, and encourage unshakable loyalty.

(4) Easier transactions: Artificial intelligence, the Internet of Things (IoT), and blockchain technology will enable real-time, secure, and transparent transactions for FinTech firms worldwide. Enterprises will be able to boost their efficiency by utilizing automation and secure peer-to-peer transactions for digital payments, loan origination and servicing, BNPL, digital lending, and other applications.

(5) Permanent service: Data will be stored on dispersed nodes as a result of decentralization, which would dramatically reduce account suspensions and denial of distributed services in Web 3.0. Furthermore, this will help FinTech companies reduce the expense of dealing with server failures or seizures.

In summary, with the internet of things and blockchain technology, we are going to see a major shift in the way that Fintech is delivered. That means more convenience for customers and lower costs for banks. It also means that there will be less need for middlemen like brokers who take a cut of your trades or platforms like Robinhood which charge fees when you trade stocks directly through their app instead of using an intermediary broker. The future is bright!